Table of Contents >> Show >> Hide

- The classic 60/40 portfolio: why it became the default

- Enter 60/30/10: adding a permanent cash sleeve

- Behavior vs. optimization: the real battleground

- Pros and cons of adding a 10% cash sleeve

- Who might prefer 60/30/10 over 60/40?

- How to build a 60/30/10 portfolio in practice

- Real-world experiences with 60/30/10 vs. 60/40

- Conclusion: should you go 60/30/10 instead of 60/40?

For decades, the classic 60/40 portfolio (60% stocks, 40% bonds) has been the Toyota Corolla of investing: not flashy, not perfect, but solid, boring, and surprisingly hard to beat. Lately, though, more investors have been asking a very reasonable question:

“What if I keep 10% in cash and go with a 60/30/10 portfolio instead?”

This idea was popularized in a post on the blog A Wealth of Common Sense, where Ben Carlson explored whether a permanent 10% cash sleeve would meaningfully hurt returns or simply help people sleep at night. Spoiler: the answer lives at the intersection of math and psychologywhere spreadsheets meet feelings.

In this deep dive, we’ll compare 60/30/10 vs. 60/40, look at what the data says, talk through the trade-offs, and figure out who might benefit from a cash-heavy twist on the traditional balanced portfolio.

The classic 60/40 portfolio: why it became the default

A 60/40 mix is the default asset allocation in textbooks, target-date funds, and countless model portfolios. The idea is simple:

- 60% stocks for long-term growth.

- 40% bonds for income and ballast when stocks stumble.

Historically, that combo has done its job. Vanguard’s research on a global 60/40 portfolio shows that even including the ugly year of 2022when both stocks and bonds fell hardthe long-term annualized return over the past decade was still around the high-6% range, in line with its long-run average.

Morningstar’s 150-year stress test of a 60/40 portfolio finds that, across wars, depressions, inflation shocks, and rate cycles, a balanced stock–bond mix has historically delivered strong risk-adjusted returns. Even during brutal crashes like 1929, diversified stock/bond portfolios typically fell far less than an all-equity allocation.

So why all the drama lately about 60/40 being “dead”?

Because the last few years have been rough. The 2022–2023 period delivered one of the worst stretches for 60/40 in roughly 150 years, largely thanks to a historic bear market in bonds. When interest rates spiked from near-zero to “oh wow, that’s real yield,” bond prices sank, and for once, bonds didn’t provide their usual cushion when stocks dropped.

Yet even after that, big asset managers like Vanguard and Morningstar still argue that 60/40 remains a perfectly reasonable starting point for investors with moderate risk tolerance. What’s changed is that more people are questioning whether they personally can ride out the bumps without panicking.

Enter 60/30/10: adding a permanent cash sleeve

This is where the 60/30/10 portfolio comes in:

- 60% stocks

- 30% bonds

- 10% cash (or cash-like: money market funds, T-bills, high-yield savings)

Long-run average returns often get summarized as something like:

- Stocks: ~9–10% per year

- Bonds: ~4–5% per year

- Cash: ~2–3% per year

These are ballpark U.S. historical numbers based on large-cap stocks, investment-grade bonds, and short-term Treasury bills. Cash clearly has the lowest expected return of the three, so on paper, adding a permanent 10% cash slice should drag down long-term performance.

What the numbers say about 60/30/10 vs. 60/40

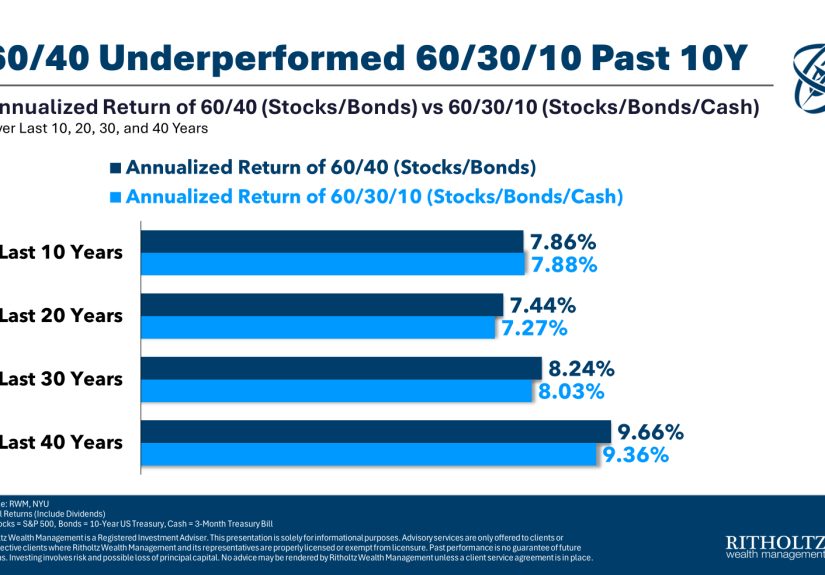

In the original A Wealth of Common Sense analysis, Carlson compared 60/40 and 60/30/10 over the 10, 20, 30, and 40 years through 2023. Over the full 40-year window, 60/40 did come out ahead, as you’d expectbonds simply outperformed cash over that long horizon. But the difference in annual return wasn’t enormous.

The plot twist? Over the most recent 10-year period, the cash-heavy 60/30/10 portfolio actually outperformed 60/40, thanks to the epic bond bear market and rising short-term rates. Bonds were crushed as yields rose, while cash yields adjusted upward far faster.

Zooming out, the conclusions look something like this:

- Over very long horizons: 60/40 tends to win, but not by a massive margin.

- Over recent bond-stress periods: 60/30/10 can look surprisingly strong, sometimes even better.

- Volatility and drawdowns: The 60/30/10 portfolio generally experiences smoother rides, because that 10% cash is rock steady.

In other words, you are paying a modest potential performance cost, mostly visible over multi-decade horizons, in exchange for a calmer ride and more emotional comfort.

Behavior vs. optimization: the real battleground

If investing were purely a math contest, we’d all run an optimized, factor-tilted, tax-loss-harvested, multi-asset strategy that only quants can pronounce. In reality, most people are human (tragic, but there it is).

Carlson’s core point is that a “suboptimal strategy you can stick with” beats an “optimal strategy you abandon”. That theme echoes across investor behavior research: people routinely bail at the worst times, especially when portfolios fall more than they emotionally expected.

A 10% cash buffer can act as a behavioral release valve:

- You see a market drop and think, “At least I have dry powder; I don’t have to sell.”

- You’re less likely to feel cornered into panic-selling stocks or bonds.

- You know you have months (or years) of expenses in safe assets, which can be huge for retirees.

That psychological breathing room can be worth more than the slight expected-return penalty. If 10% in cash helps you stay invested in the other 90% through scary markets, the behavioral win can easily outweigh the mathematical drag.

Pros and cons of adding a 10% cash sleeve

Upsides of the 60/30/10 portfolio

-

Lower volatility and shallower drawdowns.

Cash doesn’t move much (in price), so a permanent 10% allocation softens both gains and losses. During years like 2022when both stocks and bonds fellcash was a rare bright spot as yields surged. -

Dry powder for opportunities.

Holding cash gives you optionality. If stocks or bonds cheapen dramatically, you have ready capital to rebalance aggressively without selling something else at a bad time. -

Better sleep quality.

If you’re retired or close to it, knowing that 10% of your portfolio is in boring, predictable vehicles (money markets, T-bills, etc.) can make market volatility more tolerable. -

A smoother behavioral ride.

You’re less likely to smash the “sell everything” button if your portfolio is a bit more conservative than the standard textbook mix.

Downsides and trade-offs

-

Lower expected long-term returns.

Over multi-decade periods, bonds have historically outpaced cash, and stocks have outpaced both. That 10% in cash is very likely to earn less than if it sat in stocks or high-quality bonds. -

Inflation risk.

Cash feels safe, but over long stretches inflation quietly eats into its purchasing power. If inflation runs hotter than your cash yield, your “safe” money loses real value over time. -

Regret in strong bull markets.

When stocks and bonds soar in tandemas they did in parts of 2023–2024a 10% cash reserve can make your returns lag a pure 60/40 portfolio. That’s the price of risk reduction.

There’s no free lunch: you’re trading a bit of headline performance for more emotional safety and flexibility.

Who might prefer 60/30/10 over 60/40?

A 60/30/10 mix won’t be ideal for everyone, but it can make a lot of sense for certain types of investors:

- Nervous first-time investors. If you’re new to markets and terrified of watching your portfolio drop 25% in a year, starting with a slightly more conservative 60/30/10 can help you build confidence.

- Pre-retirees and new retirees. If you’re within about 5–10 years of retirement or just started withdrawing, reducing volatility and sequence-of-returns risk can matter more than squeezing out an extra 0.3% per year.

- Investors with lumpy cash needs. Planning for a home purchase, tuition, or a business opportunity? A built-in cash sleeve can keep you from cannibalizing your long-term investments.

- People who know they’re emotionally reactive. If you’ve rage-sold during past corrections, you probably don’t need more leverage; you need a structure that keeps your future self from doing something dramatic.

On the other hand, long-horizon investors who are comfortable with volatilityespecially younger investors with stable incomesmay still prefer a traditional 60/40 or even more aggressive allocations like 70/30 or 80/20.

How to build a 60/30/10 portfolio in practice

The good news: building a 60/30/10 portfolio doesn’t require exotic products. Low-cost U.S. investors often do something like:

- 60% stocks – a broad U.S. or global index fund (for example, a total stock-market ETF).

- 30% bonds – a core bond fund covering Treasuries and investment-grade corporates.

- 10% cash – high-yield savings, money market funds, short-term Treasury bills, or a cash management account.

From there, you simply:

- Pick your funds or ETFs, prioritizing low fees and broad diversification.

- Set target weights (60/30/10).

- Rebalance once or twice a year, nudging each sleeve back toward its target.

Some investors go further and add alternative assetssuch as trend-following strategies, real assets, or hedge-fund-like liquid alternativeson top of a 60/40 or 60/30/10 base. Research from CFA Institute, BlackRock, and others suggests that modest allocations to thoughtfully chosen alternatives can reduce drawdowns and improve risk-adjusted returns, even if headline returns don’t skyrocket.

But you don’t have to complicate things. For many people, the real upgrade isn’t altsit’s finally landing on a simple allocation they can live with.

Real-world experiences with 60/30/10 vs. 60/40

Let’s talk about how this actually feels in real life, beyond the neat backtests.

A decade of bond pain and cash’s surprise glow-up

Over the decade leading into the mid-2020s, bonds had a rough run, capped by what many analysts called the worst bond bear market in modern history. When rates rose rapidly from near-zero, longer-term Treasuries and core bond funds posted deep losses. At the same time, short-term yields on cash and T-bills reset higher4% or more wasn’t unusual in U.S. money market funds.

That meant investors with a 60/30/10 allocation experienced a very different emotional arc than classic 60/40 investors:

- 60/40 investors watched both the stock and bond sides of their statement bleed at the same time“wait, even my ‘safe’ part is down?”

- 60/30/10 investors saw painful declines too, but that 10% in cash sat there quietly, earning higher yields and acting as visible stability on the page.

Anecdotally, advisors report that clients with explicit cash buckets or sleeves tended to feel less betrayed by their “safe” assets and were more willing to stick to their plan or rebalance into weakness. That behavioral differencewho stayed the course vs. who bailedis where the cash sleeve earns its keep, even if the spreadsheet doesn’t immediately show it.

Three composite investor stories

To bring this down to earth, imagine three (fictional but realistic) investors:

- Case 1 – Maya, age 62: She’s five years from retirement and has accumulated a decent nest egg but is terrified of a “2008 right before I quit” scenario. Her advisor moves her from 60/40 to 60/30/10, framing the 10% cash as 1–2 years of breathing room if markets tank. When 2022 hits, Maya hates the losses, but seeing that cash sleeve gives her enough confidence to stay invested. A pure 60/40 might have pushed her over the edge into panic-selling.

- Case 2 – Jordan, age 35: He’s aggressive, has stable income, and likes to tinker. For him, 60/30/10 is probably unnecessary. He can tolerate an 80/20 mix and sees the cash drag as a long-term cost with little emotional benefit. A traditional (or even more aggressive) allocation makes sense given his horizon and temperament.

- Case 3 – Lee & Sam, early retirees: They live off a 3–4% withdrawal rate and constantly worry about sequencing riskbad returns early in retirement. A 60/30/10 framework aligns well with a “bucket” strategy: cash for near-term spending, bonds for the next several years, and stocks for long-term growth. That clear mental map helps them avoid cutting spending or abandoning their plan after a rough year.

None of these stories prove 60/30/10 is universally better than 60/40it isn’t. What they illustrate is that the “right” portfolio is deeply personal. The ideal mix isn’t just about maximizing expected returns; it’s about maximizing the odds that you will actually follow your plan through full market cycles.

Why “good enough and durable” beats “perfect and fragile”

The recurring lessonfrom academic papers to advisor experienceis that staying invested is the real superpower. A slightly less efficient portfolio that you stick with for 30 years will usually beat a theoretically optimal one that you abandon every time the market scares you.

If a permanent 10% cash sleeve:

- helps you survive brutal years like 2022,

- keeps you from selling at the bottom, and

- gives you the confidence to rebalance when everything looks bleak,

then 60/30/10 isn’t a “wimpy” version of 60/40it’s a customized, behavior-friendly upgrade for the specific investor who needs that safety valve.

Conclusion: should you go 60/30/10 instead of 60/40?

On paper, 60/40 still makes a lot of sense. It has a long history of solid returns and reasonable volatility, and recent analysis from firms like Vanguard, Morningstar, and others suggests its long-term prospects remain viable, especially now that bond yields are no longer microscopic.

But in the real world, investing isn’t done on paperit’s done with human emotions, messy lives, and imperfect discipline. A 60/30/10 portfolio acknowledges that:

- You might trade a small slice of long-term return.

- In exchange, you get more liquidity, smoother performance, and better odds of staying the course.

If that 10% cash sleeve is the difference between you panicking in the next bear market or calmly rebalancing, it’s not a bugit’s a feature. The key is to choose the mix that lines up with your goals, risk tolerance, and temperament, and thenthis is the hard partactually stick with it.

There’s no magic ratio that works for everyone. But asking “what about 60/30/10 instead of 60/40?” is exactly the kind of common-sense question more investors should be asking: not “what’s perfect?” but “what’s realistic for me?”