Table of Contents >> Show >> Hide

- What Is a Credit Utilization Ratio?

- Why Credit Utilization Matters So Much

- How to Calculate Your Credit Utilization Ratio Step by Step

- How to Calculate Utilization on a Single Card

- What Is a Good Credit Utilization Ratio?

- Statement Balance vs. Current Balance: The Timing Trap

- Common Mistakes When Calculating Credit Utilization

- How to Lower Your Credit Utilization Ratio

- Quick Examples You Can Copy

- Real-World Experiences: What Credit Utilization Feels Like in Everyday Life

- Final Takeaway

- SEO Tags

Note: Body-only HTML, English content, web-publishing ready, with SEO JSON at the end.

Credit utilization ratio sounds like one of those phrases invented to make normal people close their laptops and go stare at a wall. But it is actually simple, incredibly important, and surprisingly useful if you want to improve your credit score without selling a kidney or becoming a spreadsheet monk.

In plain English, your credit utilization ratio tells lenders how much of your available revolving credit you are using. If your cards are your financial toolbox, utilization shows whether you are responsibly borrowing a screwdriver or trying to walk off with the whole hardware aisle. Because credit scoring models pay close attention to this number, learning how to calculate it can help you make smarter decisions about balances, payments, and even the timing of when you pay.

This guide breaks down exactly how to calculate your credit utilization ratio, what counts in the formula, what percentage is considered healthy, and how to lower it if yours looks a little too spicy.

What Is a Credit Utilization Ratio?

Your credit utilization ratio is the percentage of your available revolving credit that you are currently using. The keyword here is revolving. That usually means credit cards and other revolving lines of credit, not installment loans like mortgages, auto loans, student loans, or most personal loans.

Here is the basic formula:

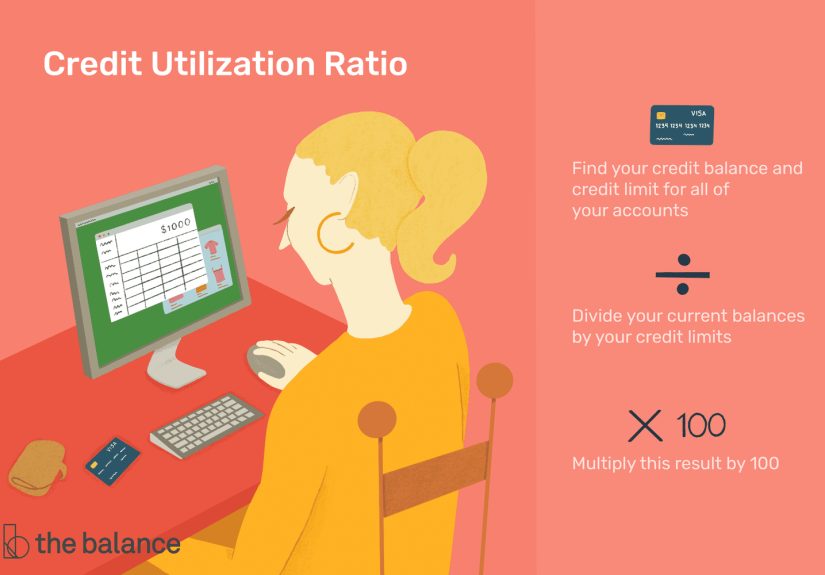

Credit Utilization Ratio = (Total Revolving Balances ÷ Total Revolving Credit Limits) × 100

That percentage gives lenders and credit scoring models a snapshot of how heavily you are leaning on your existing credit lines. Lower percentages are generally better. A very high ratio can make it look like you may be overextended, even if you have never missed a payment.

Why Credit Utilization Matters So Much

Credit utilization is one of the most important parts of your credit profile because it falls under the “amounts owed” category in widely used scoring models. Translation: the number matters, and it matters more than many people realize.

Payment history is still king, but utilization is often the fastest-moving factor you can improve. You cannot magically make your credit history ten years older by next Tuesday. But you can lower a card balance before the statement closes. That is why utilization is often the first lever people pull when they want to see credit score improvement in a relatively short period.

A high ratio can signal risk. A low ratio can signal control. And in personal finance, “I have this under control” is a message worth sending.

How to Calculate Your Credit Utilization Ratio Step by Step

Step 1: List every revolving account

Gather your credit cards and any other revolving lines of credit that report balances and limits. Look at your latest statements or online account dashboards.

Step 2: Write down each balance

Use the most recently reported or statement balance if you want a number that is closest to what may appear on your credit report. Your current balance may be different if you have made new purchases or payments since the statement date.

Step 3: Write down each credit limit

This is the maximum amount available on each revolving account.

Step 4: Add all balances together

This gives you your total revolving balance.

Step 5: Add all credit limits together

This gives you your total available revolving credit.

Step 6: Divide balances by limits and multiply by 100

The result is your overall utilization percentage.

Example: Overall utilization

- Card A: $500 balance, $2,000 limit

- Card B: $1,200 balance, $3,000 limit

- Card C: $0 balance, $5,000 limit

Total balances = $1,700

Total limits = $10,000

$1,700 ÷ $10,000 = 0.17

0.17 × 100 = 17%

Your overall credit utilization ratio is 17%.

How to Calculate Utilization on a Single Card

You should also calculate utilization for each card individually. Why? Because one heavily used card can still raise eyebrows even if your total utilization looks fine.

Single-Card Utilization = (Card Balance ÷ Card Limit) × 100

Example:

- One card balance: $900

- Credit limit: $1,000

$900 ÷ $1,000 = 0.90

0.90 × 100 = 90%

That card is at 90% utilization, which is very high. Now imagine you also have another unused card with a $9,000 limit. Your total utilization would be just 9%, which looks excellent overall. But that first card is still nearly maxed out. Some scoring models notice both the total picture and the per-card picture, so it is smart to monitor both.

What Is a Good Credit Utilization Ratio?

The classic rule of thumb is to keep utilization below 30%. That is the benchmark you will hear most often because it is simple, practical, and better than drifting into the danger zone.

But here is the more nuanced truth: lower is generally better, as long as you are using credit normally and responsibly. Many people with excellent credit scores keep utilization in the single digits. That does not mean you need to panic if you hit 12% one month. It just means that 29% is not some magical VIP lounge where the best scores hang out eating complimentary almonds.

A useful way to think about it:

- 0% to 9%: Excellent range for many borrowers

- 10% to 29%: Generally considered good

- 30% and up: May start hurting your scores

- 50% and up: Risky territory

- Near maxed out: Big red flag

Also, zero is not always the holy grail people think it is. If every card reports a zero balance all the time, you may miss the small benefit that can come from showing active but lightly managed revolving credit.

Statement Balance vs. Current Balance: The Timing Trap

One of the most frustrating parts of credit utilization is that the number on your credit report may not match what you see in your banking app today. That is because many card issuers report balances around the end of your billing cycle, often when your statement closes, not necessarily after you pay the bill due later.

So yes, you can pay your card in full every month and still have a balance report to the credit bureaus. Annoying? Absolutely. Normal? Also yes.

Example:

- Credit limit: $4,000

- Statement closes with a balance of $2,000

- Utilization reported: 50%

- You pay the full $2,000 by the due date and avoid interest

Financially, you did great. Scoring-wise, the reported utilization may still look high until the next reporting cycle updates your balance. That is why people preparing for a mortgage, auto loan, or major financing often pay balances down before the statement closing date, not just before the due date.

Common Mistakes When Calculating Credit Utilization

Including installment loans

Your mortgage, car loan, and student loan balances are important to your credit profile, but they are not part of your standard revolving credit utilization calculation.

Looking at only one card

A single-card ratio matters, but so does your total ratio across all revolving accounts.

Ignoring statement dates

If you only pay by the due date, your reported utilization may still be higher than expected.

Closing an old card too quickly

Closing a credit card can reduce your total available credit. If your balances stay the same while your limits shrink, your utilization ratio rises. That can hurt your score even if your spending did not change at all.

Thinking 30% is the target

Below 30% is usually better than above 30%, but it is not a finish line ribbon. Lower often helps more.

How to Lower Your Credit Utilization Ratio

Pay down balances before the statement closes

This is one of the most effective moves because it can lower the balance that gets reported.

Make multiple payments each month

Small mid-cycle payments can keep balances from ballooning.

Ask for a credit limit increase

If your issuer raises your limit and your balance stays the same, your utilization drops automatically. Just make sure the higher limit does not become an invitation to shop like you are starring in a game show.

Spread charges across cards

This can help prevent one card from showing extremely high utilization.

Keep useful older cards open

Especially if they have no annual fee and are not causing problems, they can help support your total available credit.

Use credit strategically before applying for a loan

If you are planning to apply for a mortgage, refinance, or auto loan, try to get reported balances as low as possible a month or two ahead of time.

Quick Examples You Can Copy

Example 1: One card

Balance: $300

Limit: $1,500

$300 ÷ $1,500 × 100 = 20%

Example 2: Two cards

Card 1: $400 balance, $2,000 limit

Card 2: $600 balance, $3,000 limit

Total balances: $1,000

Total limits: $5,000

$1,000 ÷ $5,000 × 100 = 20%

Example 3: High card, low overall

Card 1: $900 balance, $1,000 limit = 90%

Card 2: $0 balance, $9,000 limit = 0%

Overall: $900 ÷ $10,000 × 100 = 9%

Lesson: your total ratio can look beautiful while one card quietly screams for help.

Real-World Experiences: What Credit Utilization Feels Like in Everyday Life

Credit utilization is one of those personal finance ideas that sounds tiny on paper but feels huge in real life. People often discover it not in a textbook, but in a slightly panicked moment after checking a credit score and wondering why it dipped even though every payment was made on time. That is usually the moment utilization walks into the room wearing sunglasses and acting important.

A common experience goes like this: someone uses one rewards card for everything because it earns solid cash back, keeps another card in a drawer for emergencies, and pays the full balance every month. Financially, that person is doing plenty right. But if the main card reports a high statement balance before payment clears, the credit report may show a utilization spike. Suddenly, a responsible spender feels like they failed some secret exam they did not know they were taking.

Another very normal experience happens during a big purchase month. Maybe a family books travel, replaces a broken appliance, or buys school supplies, and the total on one card jumps from “cute little balance” to “oh wow, that escalated quickly.” Even if the cash exists to pay the bill, the reported balance can temporarily push utilization above 30% or even 50%. The score dip feels personal, but it is usually just math reacting to timing.

Then there is the “I closed a card to be responsible” story. Someone gets rid of an unused account, feels organized and emotionally mature, and then finds out their utilization ratio rose because their total available credit shrank. It is one of the most irritating plot twists in consumer finance. You try to clean the house, and the credit score complains that you moved the furniture.

There are also positive experiences. Many borrowers report that once they start paying attention to statement closing dates instead of only payment due dates, the whole system makes more sense. They begin making one extra payment mid-month, or they pay down a large purchase before the statement prints, and their utilization improves without any dramatic lifestyle change. That realization can feel empowering because it turns credit from a mystery into a process.

The biggest lesson from real-life utilization experiences is this: a credit score is not judging your soul. It is reacting to reported balances, available limits, and patterns. When you understand how those pieces work together, you stop treating utilization like random punishment and start treating it like a tool. And tools are much less scary when you know which end to hold.

Final Takeaway

Calculating your credit utilization ratio is not difficult, but understanding it can make a real difference in your financial life. Add up your revolving balances, divide by your total revolving limits, and multiply by 100. Then check the same math on each card individually.

If your ratio is high, do not panic. Utilization is one of the more flexible parts of your credit profile. Lower balances, smarter timing, and a little attention to statement dates can go a long way. Think of it as financial housekeeping: not glamorous, occasionally annoying, but very effective when company is coming and by company, we mean lenders.

The goal is not perfection. The goal is control. Once you know how to calculate your credit utilization ratio, you are no longer guessing. You are managing.