Table of Contents >> Show >> Hide

- What “Long-Term Inflation Outlook” Actually Means (No, It’s Not a Fortune Cookie)

- Why Our Long-Term Outlook Is Improving

- 1) Headline inflation has cooled, and underlying measures are less alarming than before

- 2) Market-based long-run inflation signals look close to “anchored” territory

- 3) Survey-based expectations look steadier in the longer horizons

- 4) The Fed’s credibility and framework still act like an anchor

- 5) Supply-side healing and normalization effects are still helping

- The “Sticky” Part: Why We’re Not Declaring Victory Yet

- What Could Still Re-Ignite Inflation Long-Term?

- Specific Examples: What “Improving Long-Term Inflation” Looks Like in Real Life

- What We’re Watching Next (Because Inflation Loves Plot Twists)

- Conclusion: Better Doesn’t Mean PerfectBut It Does Mean More Manageable

- Experiences: Real-World Snapshots of an Improving Inflation Outlook (Illustrative)

For the last few years, inflation has been the economic equivalent of that one group chat member who won’t stop texting: loud, persistent, and somehow always popping up right when you’re trying to relax. But lately, the signal has been getting quieterand not just in “please, let this be true” vibes. A growing stack of data, surveys, and market signals suggests the long-term inflation picture in the United States is looking more stable than it did when price tags were doing parkour.

“Improves” doesn’t mean inflation vanishes into a magical mist. It means the odds are rising that inflation settles closer to the Federal Reserve’s 2% goal over time, and that long-run expectations remain anchored instead of drifting upward and turning every wage negotiation into a sequel. The story is still complicatedbecause economics is never allowed to be simplebut the long-term trend lines are finally acting like they remember the rules.

What “Long-Term Inflation Outlook” Actually Means (No, It’s Not a Fortune Cookie)

When economists talk about the “long-term outlook” for inflation, they’re not predicting next month’s grocery bill like it’s a weather forecast. They’re looking at whether inflation expectations and underlying price pressures point to a multi-year path that settles into something sustainablethink “boring and predictable,” which is the highest compliment in macroeconomics.

The long-term outlook matters because expectations can become self-fulfilling. If businesses and workers believe inflation will run hot for years, prices and wages can start behaving that waymaking it harder for inflation to come down without major economic pain. That’s why central banks obsess over whether expectations are “well anchored.”

Three big ways we gauge long-term inflation expectations

- Market-based expectations (like Treasury Inflation-Protected Securities, aka TIPS, and breakeven inflation rates).

- Consumer surveys (like the New York Fed’s Survey of Consumer Expectations and the University of Michigan survey).

- Official projections and frameworks (like the Fed’s longer-run goals and the Congressional Budget Office outlook).

No single measure is perfect. Markets react fast (sometimes too fast). Surveys capture lived sentiment (sometimes too dramatically). Official projections are careful (sometimes too careful). But when multiple gauges point in the same direction, the confidence level improvesand right now, several are pointing toward a steadier long-term inflation path.

Why Our Long-Term Outlook Is Improving

1) Headline inflation has cooled, and underlying measures are less alarming than before

Recent inflation prints show a meaningful downshift from the peak era, and importantly, some of the “trend” measures that filter out noisy categories suggest inflation is no longer in full sprint. The Consumer Price Index (CPI) has been running far below the peak rates seen in 2022, and the Personal Consumption Expenditures (PCE) price indexthe Fed’s preferred inflation gaugehas also eased compared with the worst period.

Even better (for the “please let this be normal again” crowd), trimmed-mean and median measuresdesigned to strip out the craziest price movesshow inflation pressure is less broad-based than it was when everything from eggs to airline tickets felt like it was priced by a prankster.

2) Market-based long-run inflation signals look close to “anchored” territory

One of the most watched indicators is the 5-year, 5-year forward inflation expectation rate. It’s basically the market’s estimate of average inflation over a five-year period that starts five years from now. Translation: “What do investors think inflation will look like once the near-term chaos is long gone?”

Lately, that forward measure has been hovering a little above 2%suggesting investors largely expect inflation to behave in a way that’s consistent with the Fed’s long-run goal. That doesn’t mean markets are certain. It does mean the market narrative has shifted away from “inflation forever” and toward “inflation, but make it manageable.”

The 10-year breakeven inflation rate has also been sitting in a range that implies markets expect inflation around the low-to-mid 2% neighborhood over the next decadeagain, not perfect, but far less scary than the “everything is on fire” phase.

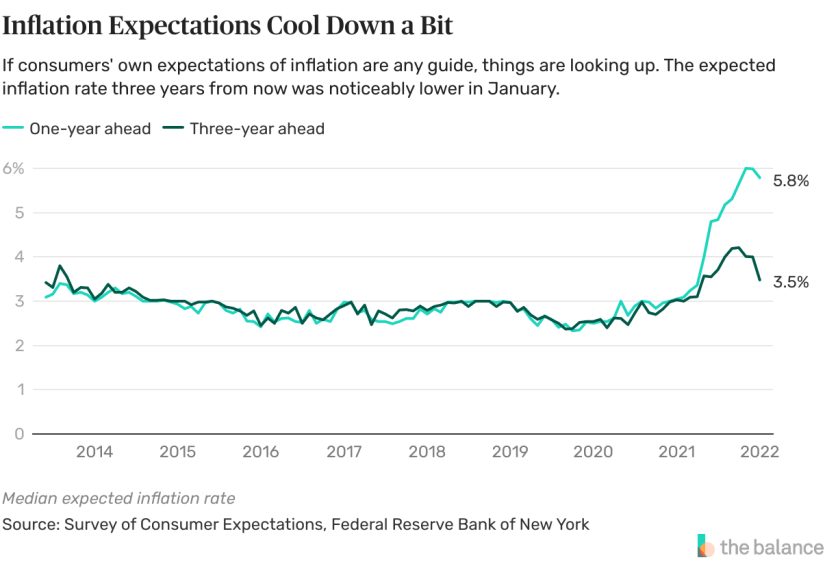

3) Survey-based expectations look steadier in the longer horizons

The New York Fed’s Survey of Consumer Expectations often shows that near-term inflation expectations swing with gas prices, grocery prices, and whatever consumers argued about at the checkout line. But the longer horizons3-year and 5-year expectationstend to be steadier, and that stability matters for long-term inflation psychology.

Meanwhile, University of Michigan data has shown long-run expectations have moved around, sometimes spiking during periods of policy uncertainty or price shocks, but they’ve also shown the ability to cool from peaksan important sign that inflation expectations aren’t unmooring permanently.

Put differently: people may still feel inflation in their bones when they buy snacks at an airport, but many aren’t assuming it will stay wild forever. That’s a meaningful improvement.

4) The Fed’s credibility and framework still act like an anchor

The Federal Reserve explicitly targets 2% inflation over the longer run and has repeatedly emphasized the importance of keeping longer-term expectations anchored. That commitmentplus the reality of policy tightening when inflation surgedhas reinforced the idea that the central bank will respond if inflation threatens to re-accelerate.

In plain English: people believe the Fed is willing to do the annoying thing (higher rates, slower growth) if that’s what it takes to prevent inflation from becoming a permanent lifestyle.

5) Supply-side healing and normalization effects are still helping

A chunk of the inflation surge came from supply chain disruptions, product shortages, and sudden demand shifts. As shipping and inventory dynamics normalized, goods inflation cooled. That’s not a one-time miracle, but it does reduce the probability that the economy is stuck in a structural “shortages everywhere” regime.

Long-term inflation is usually less about one-off shocks and more about persistent imbalanceslike overheated demand, chronic labor shortages, or ongoing policy-driven cost pressures. The fact that some of the earlier inflation drivers have faded improves the baseline long-term outlook.

The “Sticky” Part: Why We’re Not Declaring Victory Yet

If inflation were a movie, “sticky inflation” would be the sequel nobody asked for but keeps getting greenlit. Some prices adjust slowlyespecially servicesand those can keep inflation elevated even when goods prices calm down.

Measures like the Atlanta Fed’s Sticky-Price CPI help capture that slower-moving part of inflation. Sticky inflation tends to reflect underlying pressures like wages, rent dynamics, and demand for services. The good news is that even when sticky components are elevated, their trend can still soften over time. The not-as-fun news is that sticky inflation is the part most likely to resist a quick return to 2%.

Housing: the inflation category that refuses to stop being important

Housing-related inflation (rent and owners’ equivalent rent in CPI, and housing services in broader frameworks) can be slow to turn because leases roll over gradually and measurement is designed to capture ongoing costs, not instant changes. The long-term outlook improves if housing inflation cools sustainablywhich tends to happen when new supply comes online and rent growth slows.

This is where “long-term” is key. Even if monthly readings bounce around, the multi-year direction matters more than whether rent was slightly weird in one city for two months.

What Could Still Re-Ignite Inflation Long-Term?

Improved outlook doesn’t mean “risk-free.” Inflation is like glitter: even when you think it’s gone, you’ll find a little more lateron the couch, in your hair, and in your macro forecast.

1) Energy shocks and geopolitics

Oil and energy prices can surge due to conflicts or supply constraints. Even if the Fed focuses on core inflation, sustained energy spikes can seep into transportation costs, production costs, and household expectations. Markets can react quickly, and consumers notice it immediately at the pump.

2) Trade policy and tariffs

Tariffs can raise input costs and consumer prices, at least in the near to medium term, depending on how businesses absorb or pass through those costs. If tariff-related price pressures persistor if they trigger expectation shifts they can complicate the disinflation path.

3) Fiscal dynamics and demand pressure

Large deficits don’t automatically cause inflation, but sustained fiscal stimulus in an economy near capacity can add demand pressure. The long-term inflation outlook is better when demand growth and supply capacity stay reasonably aligned.

4) Labor market imbalances

Wage growth that consistently outruns productivity can push service-sector prices higher. That doesn’t mean wages are “bad” (wages are good; paying people is kind of the point). It means long-term inflation is easier to manage when wage gains are supported by productivity improvements and stable pricing power.

Specific Examples: What “Improving Long-Term Inflation” Looks Like in Real Life

Example 1: A small business resets pricing behavior

During peak inflation, a local café might have raised prices multiple times a year because milk, coffee beans, cups, and labor costs were all moving fast. In a more stable long-term environment, the café is more likely to return to “annual menu updates” rather than “surprise price roulette.”

Example 2: Consumers stop assuming every price jump is permanent

When people believe inflation will stay high, they may accelerate purchases (“buy now before it gets worse”)which can add demand and keep inflation sticky. When long-term expectations are steadier, consumers are less likely to act like every purchase is a timed escape room.

Example 3: Long-term contracts get easier to write

In a low-and-stable inflation world, businesses can sign multi-year supplier contracts or lease agreements with less fear that costs will explode unpredictably. That helps investment planning and can reduce the “inflation risk premium” that sneaks into pricing.

What We’re Watching Next (Because Inflation Loves Plot Twists)

- Core PCE trend: still the Fed’s main scoreboard for underlying inflation.

- Sticky vs. flexible inflation: whether slower-moving services pressures cool further.

- Long-run expectations: especially market-based forward measures and 5–10 year survey horizons.

- Housing and labor: rent dynamics and wage growth relative to productivity.

- Policy shocks: energy, tariffs, and fiscal changes that could reheat prices.

The most encouraging sign isn’t a single month of good inflation data. It’s the broad sense that long-run expectations are not spiraling upwardeven after a historic inflation shock. That kind of resilience is exactly what “improving long-term outlook” looks like.

Conclusion: Better Doesn’t Mean PerfectBut It Does Mean More Manageable

Our long-term outlook on inflation improves because multiple independent signalsofficial data, market-based expectations, and consumer surveyssuggest inflation is more likely to settle into a lower, steadier range than it looked like during the peak period. The Fed’s framework and credibility help keep expectations anchored, while post-pandemic normalization has reduced some of the biggest structural pressures that drove inflation higher.

Risks remain. Energy shocks, trade policy, fiscal dynamics, and sticky services inflation can all complicate the path. But the difference now is that long-run expectations and market pricing imply “inflation that cools and stabilizes” is a more plausible base case than “inflation that stays permanently hot.”

In other words: inflation may still occasionally jump out from behind a couch and yell “BOO!”but it’s less likely to move in permanently and start charging rent.

Experiences: Real-World Snapshots of an Improving Inflation Outlook (Illustrative)

I don’t have personal shopping receipts (no pockets, no wallet, no impulse-buy gum at checkout), but we can still talk about “experiences” in a useful way: what households and businesses typically notice when inflation’s long-term outlook improves. Below are composite, realistic snapshotsbased on how inflation shows up in everyday decisions and how expectations shape behavior.

1) The “Grocery Cart Reality Check” Moment

A common experience over the last couple of years has been the mental math spiral in the cereal aisle: “Was this always $6?” When long-term inflation expectations start to stabilize, people often report a subtle shift in psychology. They still notice higher prices than pre-pandemic levels (that part doesn’t magically rewind), but they stop expecting a new surprise every week.

Practically, that looks like fewer “stock-up because it’ll be worse next month” trips. It’s not that shoppers become carefree; they become less defensive. They switch from panic-planning to normal planning: buying what they need, watching sales, and trusting that the price of a staple won’t double just because it’s Tuesday.

2) The Renter’s Slow-Burn Relief

Rent is one of the biggest “lived inflation” categories because it’s large, frequent, and impossible to ignore. When housing inflation cools, the experience isn’t always a dramatic drop in rent. More often, it’s a change in the rate of increase: renewals go from “yikes” to “okay, that’s annoying but survivable.”

Over time, slower rent growth changes behavior. Renters feel less pressured to move every year in search of affordability. Landlords and property managers become less aggressive about pushing large increases because vacancy risk matters again. And households can plan: they can commit to a budget without assuming housing costs will jump unpredictably.

3) Small Businesses Stop Pricing Like They’re Dodging Lightning

Talk to enough small business owners and you’ll hear the same story from peak inflation: cost inputs were changing so fast that pricing felt like guesswork. When the long-term outlook improves, the experience becomes less frantic. Owners still face cost changesbecause the economy is alivebut the changes become more forecastable.

That affects everything: menu printing, supplier contracts, staffing plans, and promotions. A stable long-term inflation environment encourages businesses to compete on service and quality instead of constantly playing defense against costs. And customers notice: fewer surprise “temporary” surcharges that mysteriously become permanent.

4) The “Loan Shopping Feels Normal Again” Signal

Inflation expectations and interest rates are best friends who sometimes bring out the worst in each other. When long-run inflation expectations stabilize, long-term rates can become less volatile (not necessarily lowjust less chaotic). For households, that can make big decisions feel less like a high-stakes gamble.

Instead of “Should I lock this mortgage rate RIGHT NOW before it changes in 20 minutes?” people move toward normal comparison shopping: looking at terms, fees, and total costs without feeling like the entire market is sprinting away. That calmer decision-making environment is one of the quiet benefits of a better long-term inflation outlook.

5) Expectations Stop Amplifying the Problem

One of the most important “experiences” is invisible: how expectations affect behavior. When everyone expects prices to rise rapidly for years, the economy can develop inflation-friendly habitsfront-loading purchases, demanding larger automatic price increases, building bigger inflation cushions into contracts.

When long-term expectations look more anchored, those habits soften. Businesses become less comfortable pushing big increases “just in case.” Workers still negotiate for fair wages, but the assumed baseline becomes closer to “moderate inflation” rather than “brace for impact.” That’s how improved long-term outlooks become real: they change the way decisions are made across millions of daily transactions.

The takeaway from these snapshots is simple: a better long-term inflation outlook doesn’t mean everything gets cheap again. It means the economy becomes easier to plan around. And in personal finance and business planning, “easier to plan around” is basically the deluxe edition of stability.