Table of Contents >> Show >> Hide

- A 60-Second Snapshot (Why These Numbers Matter)

- Unemployment Rates: The Labor Market “Weather Report”

- Interest Rates: The “Price of Money” (and the Fed’s Main Dial)

- Mortgage Rates: Why Your Home Loan Doesn’t Follow the Fed Like a Pet Dog

- Credit Card Rates: Where “Convenience” Can Turn Into “Compounding”

- How These Four Rates Connect (and Why You Feel It at the Grocery Store)

- Practical “So What?”: What to Watch and What to Do (Without Overreacting)

- Common Myths (Let’s Retire These Gently)

- Putting It All Together: A Short Story in Four Rates

- Experiences: What These Rates Feel Like in Real Life (500+ Words)

- 1) The job seeker who learns that “4.3%” doesn’t mean “easy”

- 2) The homeowner who becomes an amateur meteorologist of mortgage rates

- 3) The credit card user who discovers compounding is not a personality trait

- 4) The small business owner who sees rates as a hiring decision

- 5) The household that feels fine on paper but tight in practice

- Conclusion

If the economy had a dashboard, these four gauges would be right in the middlebig, bright, and impossible to ignore.

Unemployment tells you how hard it is to land a job. Interest rates tell you how expensive it is to borrow money.

Mortgage rates tell you whether “buy a home” feels like a dream or a math problem. Credit card rates tell you whether

carrying a balance is mildly annoying or full-on wallet arson.

This article breaks down what each rate means, how it’s measured, why it moves, and how the four interactplus real-world

examples (with real numbers) so it doesn’t feel like an economics textbook fell on your head.

Quick note: This is educational information, not personalized financial advice. Rates and personal loan terms vary by borrower and lender.

A 60-Second Snapshot (Why These Numbers Matter)

Here’s the basic idea: jobs and borrowing costs feed each other. When borrowing is cheaper, businesses often invest and hire more.

When hiring is strong, households typically spend more confidently. When spending is strong, prices can rise fasterthen the Federal Reserve

may try to cool things down by raising short-term rates. That, in turn, can push up borrowing costs (including credit cards and, indirectly,

mortgages). It’s a feedback looplike a thermostat, but for the entire U.S. economy.

Where things stood in mid-February 2026 (context, not a forever promise)

- Unemployment rate (U-3): 4.3% in January 2026 (BLS). This is the headline rate you hear on the news.

- Federal funds target range: 3.50% to 3.75% as of February 19, 2026 (Federal Reserve/FRED).

- 30-year fixed mortgage average: 6.01% as of February 19, 2026 (Freddie Mac PMMS).

- Credit card interest (existing accounts average): 20.97% for November 2025 (Fed data via FRED).

- Average APR on new credit card offers: about 23.77% in February 2026 (LendingTree study).

- Weekly jobless claims: 206,000 initial claims for the week ending February 14, 2026 (U.S. Department of Labor).

Don’t memorize the numbersmemorize what they do to your life. They affect whether you get hired, what your monthly payment looks like,

and how fast a credit card balance grows if you only pay the minimum.

Unemployment Rates: The Labor Market “Weather Report”

What the headline unemployment rate actually measures

In the U.S., the official unemployment rate is commonly called U-3. It’s the share of the labor force that is unemployed

and actively looking for work. That wording matters. If someone isn’t looking (for any reason), they typically aren’t counted as unemployed.

The Bureau of Labor Statistics (BLS) produces this rate from the Current Population Survey, which is based on a monthly household survey.

U-3 vs. “the bigger picture” measures

The BLS also publishes broader measures of labor underutilization (U-1 through U-6). One you’ll often hear about is U-6,

which is broader than U-3 because it includes people who are marginally attached to the labor force and people working part-time for economic

reasons (they want full-time work but can’t get it).

Why care? Because the labor market can look “fine” on U-3 while still feeling rough for specific groups (new graduates, certain industries,

or regions). In the January 2026 BLS report, for example, the overall unemployment rate was 4.3%, while teenage unemployment was much higher

(a reminder that “average” doesn’t mean “everyone”).

Jobless claims: the weekly early-warning system

If unemployment is the monthly weather report, weekly initial jobless claims are the radarmore frequent and sometimes noisier,

but useful for spotting changes sooner. Claims measure how many people filed for unemployment insurance. They don’t capture everyone who is unemployed,

but they can signal shifts in layoffs. In mid-February 2026, initial claims were reported at 206,000 for the week ending February 14.

Why unemployment moves (and why it can lag)

Unemployment often changes after the economy has already started shifting. Businesses usually don’t hire or lay off workers the minute demand changes.

They may cut overtime, slow new hiring, or pause expansion first. That’s why unemployment can be a “lagging” indicatoruseful, but not always first to react.

Interest Rates: The “Price of Money” (and the Fed’s Main Dial)

Short-term vs. long-term rates

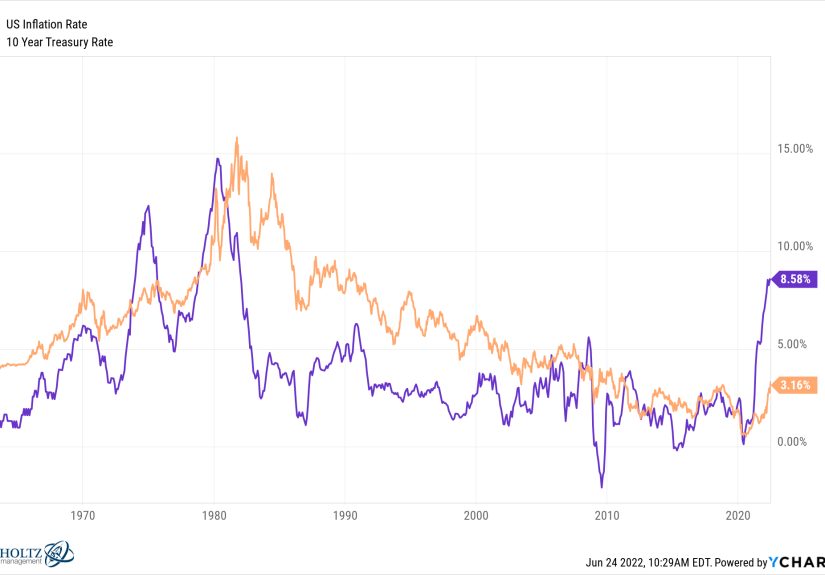

“Interest rates” is a category, not a single number. The Federal Reserve’s key policy setting is the target range for the federal funds rate,

which influences very short-term borrowing costs in the financial system. From there, short-term rates across the economy tend to move in the same direction.

Long-term rates (like 10-year Treasury yields) are shaped by expectations about inflation, growth, and future Fed policy. Mortgage rates and many business

investment decisions lean more on those longer-term expectations.

What the federal funds target range does in real life

In plain English: when the Fed keeps short-term rates higher, borrowing tends to cost more, which can cool spending and investment. When it lowers rates,

borrowing tends to get cheaper, which can boost spending and hiring (though not instantly, and not evenly).

As of February 19, 2026, the federal funds target range was 3.50%–3.75%. That number doesn’t show up on your credit card statement, but it can nudge

the rates that doespecially variable-rate products tied to benchmarks.

The prime rate: the bridge to consumer borrowing

Many consumer interest rates (especially credit cards) are built as prime rate + a margin. The prime rate typically moves in step with

Fed policy. The Consumer Financial Protection Bureau (CFPB) has emphasized that a big chunk of credit card APR behavior is about the marginmeaning card APRs

can stay high even if the prime rate drops.

Mortgage Rates: Why Your Home Loan Doesn’t Follow the Fed Like a Pet Dog

What “mortgage rates” usually means

When people talk about mortgage rates, they often mean the 30-year fixed-rate mortgage averagea standard benchmark for U.S. home loans.

Freddie Mac’s Primary Mortgage Market Survey (PMMS) is one of the most-cited sources for this weekly average.

What mortgage rates were doing in February 2026

Freddie Mac reported the 30-year fixed average at 6.01% as of February 19, 2026. That number is an average and your actual rate can vary

based on credit score, down payment, loan type, points, location, and lender pricing.

What actually drives mortgage rates

Mortgage rates are heavily influenced by longer-term market rates (especially Treasury yields) and investor expectations about inflation and future Fed policy.

Freddie Mac research has shown that much of the week-to-week movement in the 30-year fixed rate can be explained by movements in the 10-year Treasury yield.

Translation: the Fed matters, but the mortgage market cares about the whole future, not just next month.

A concrete example: what one percentage point means

Suppose you borrow $350,000 on a 30-year fixed mortgage. At 6%, the principal-and-interest payment is about $2,098/month.

At 7%, it’s about $2,329/month. That’s roughly $230/month differencebefore taxes, insurance, and HOA fees.

That “just one percent” can feel like a car payment that appears out of thin air.

Mortgage “rate” vs. APR (and why points confuse everyone)

The interest rate is the cost of borrowing. The APR (annual percentage rate) includes certain fees and can be useful for comparing loans, especially when

points are involved. If two lenders quote the same rate but one charges bigger fees, the APR will usually reveal the difference.

Credit Card Rates: Where “Convenience” Can Turn Into “Compounding”

Why credit card APRs tend to be higher than other rates

Credit cards are unsecured (no house, no car as collateral). They’re also flexibleyou can borrow, repay, and borrow again. That combination usually means

higher interest rates, because the lender is taking more risk.

Prime + margin: the two-part recipe

The CFPB often describes credit card APRs as prime rate + APR margin. In its reporting, the CFPB notes that margins have been a major

driver of high credit card rates, and that average APRs on accounts assessed interest rose sharply over the last decade.

Two “average credit card rates” that can both be true

Credit card rate headlines can look inconsistent because they’re sometimes measuring different things:

-

Existing accounts average: Fed data (via FRED) showed the commercial bank interest rate on credit card plans at 20.97%

for November 2025. -

New offers average: A LendingTree analysis reported the average APR offered with new credit card offers at about 23.77%

in February 2026.

Existing-account averages reflect what people are already paying. New-offer averages reflect what lenders are advertising to new applicants. Both matter,

but they answer different questions.

A quick balance example: the interest meter never sleeps

If you carry a $5,000 balance:

- At 20.97% APR, that’s roughly $87 of interest per month (very approximate).

- At 23.77% APR, it’s roughly $99 per month.

That’s just interestbefore you reduce the principal. It’s why paying more than the minimum can be one of the highest “returns” available in everyday life.

Why credit card rates can stay stubbornly high

Even when benchmark rates ease, card APRs may not fall much if margins stay elevated. The CFPB has highlighted that margins (the part above prime) have reached

historically high levels, which helps explain why many households still face very high borrowing costs on revolving debt.

How These Four Rates Connect (and Why You Feel It at the Grocery Store)

The chain reaction, simplified

- Fed policy rate shifts influence short-term interest rates and financial conditions.

- Borrowing costs change for businesses and consumers (credit cards often react quickly; mortgages react more indirectly).

- Spending and investment change as loans get cheaper or more expensive.

- Hiring changes as business demand changesthen unemployment follows.

Why mortgages don’t always fall when the Fed cuts

Mortgage rates are forward-looking. If investors expect inflation to be sticky or expect future growth to pick up, long-term yields may stay elevated even

if the Fed begins cutting short-term rates. On the flip side, if markets expect slower growth or lower inflation, mortgage rates can fall even before the Fed moves.

Why credit cards feel “instant”

Credit card APRs are often variable and tied to prime, so changes can pass through faster. But the margin matters too, and margins have been a major reason

card rates remain high even when other rates cool off.

Unemployment and rates: the push-pull

A strong job market can keep spending elevated, which can keep inflation pressure aliveencouraging tighter policy. A weakening job market can reduce spending,

easing inflation pressureencouraging rate cuts. That’s why economic news about jobs and inflation can move interest-rate expectations quickly.

Practical “So What?”: What to Watch and What to Do (Without Overreacting)

If you’re job hunting or planning a career move

- Don’t obsess over one month’s unemployment number. Watch the trend and also look at broader measures like underemployment and participation.

- Use weekly jobless claims as a “temperature check” for layoffs, but remember claims don’t capture every unemployed person.

-

In a slower hiring environment, your edge is specificity: tailor resumes, build a small portfolio, and lean into networking. (Yes, networking is awkward.

It’s also how jobs teleport into existence.)

If you’re buying a home or considering refinancing

- Track the 30-year fixed average for context, but shop lenders for your own quotesyour credit and loan structure matter.

- Don’t assume mortgage rates will drop just because the Fed hints at cuts. Mortgage rates follow market expectations and longer-term yields.

- Run the breakeven math on refinancing (closing costs vs. monthly savings). A lower rate isn’t “free” if fees eat the benefit.

If you’re carrying credit card debt

- Prioritize the highest APR balances first when possible. Small extra payments can shorten payoff time dramatically.

- Know your APR type: promotional APRs, variable APRs, and penalty APRs can behave very differently.

-

If you’re exploring options like balance transfers or consolidation, compare fees, promotional periods, and the post-promo APR. The goal is lower total cost,

not just a lower monthly payment.

A simple “rate-watching” routine

If you want to stay informed without doomscrolling:

- Monthly: BLS Employment Situation (unemployment rate, participation, wage trends).

- Eight times a year: Fed/FOMC decisions (policy rate direction and guidance).

- Weekly: Freddie Mac PMMS (mortgage rate trend) and jobless claims (layoff signals).

- Periodically: CFPB findings and Fed consumer credit releases for big-picture household borrowing conditions.

Common Myths (Let’s Retire These Gently)

Myth: “The unemployment rate counts everyone without a job.”

Nope. It counts people without a job who are actively looking for work and available to work. People not searching aren’t included in U-3, which is why other

measures (like U-6) can add important context.

Myth: “If the Fed cuts rates, my mortgage rate drops immediately.”

Mortgages are more tied to long-term rates and market expectations. Sometimes mortgage rates fall ahead of Fed cuts; sometimes they barely budge.

Myth: “Credit card APR is basically the Fed rate.”

Credit card APRs are typically built from a benchmark (often prime) plus a margin, and the margin can be large. That’s why card rates can stay high even

when other rates soften.

Putting It All Together: A Short Story in Four Rates

Imagine an economy where hiring is steady, unemployment is in the low-to-mid 4% range, and inflation is cooling but not fully tamed. The Fed holds its policy

range steady to avoid re-igniting inflation. Mortgage rates drift lower as investors gain confidence inflation will keep easing, but they stay meaningfully above

the ultra-low levels people remember from the past. Meanwhile, credit card APRs remain painfully high because margins are elevated and lenders price in risk.

In that world, a household can simultaneously feel “employed” and “financially squeezed.” That’s not a contradiction. It’s what happens when the job market is

okay but the cost of borrowing is still heavy. Understanding these four rates helps you spot that nuanceand make calmer decisions inside it.

500-word experiences add-on

Experiences: What These Rates Feel Like in Real Life (500+ Words)

1) The job seeker who learns that “4.3%” doesn’t mean “easy”

A common experienceespecially for new gradsis reading “unemployment is around 4%” and expecting the job hunt to feel like a fast-food drive-thru:

“Hi, I’ll take one entry-level role with benefits, please.” Then reality taps you on the shoulder. Hiring can be concentrated in certain industries, while

other sectors quietly freeze. So the headline number may look calm while your inbox looks… not calm. The practical lesson people learn is to track details:

which industries are adding jobs, how long-term unemployment is trending, and whether “part-time for economic reasons” is rising. The second lesson is emotional:

a tough job search can be real even when the national rate is relatively low.

2) The homeowner who becomes an amateur meteorologist of mortgage rates

Homeowners often describe mortgage-rate watching the way gardeners describe weather apps: compulsive, hopeful, and occasionally unhinged.

When the 30-year fixed average nudges down, people start running refinance calculators “just to see,” which is code for “I will check this six times today.”

The surprising experience is learning that the Fed can hold policy steady and mortgage rates can still movesometimes in the direction you want, sometimes

like a cat refusing to come inside. Many people eventually develop a healthier habit: they stop trying to call the exact bottom and instead watch for a range

where the savings are meaningful after fees. The win isn’t bragging about timing; it’s lowering total cost.

3) The credit card user who discovers compounding is not a personality trait

People often underestimate how fast high APRs can grow a balanceespecially when life throws a curveball (car repair, medical bill, sudden travel).

The experience is usually the same: the first month’s interest feels manageable, the second month feels annoying, and by month six the balance starts to feel

like it’s reproducing. That’s when many people notice how credit card APRs are builtprime plus a big marginand why a small policy-rate cut doesn’t suddenly

make revolving debt cheap. The most common “aha” moment is realizing that paying a little extra each month isn’t just “responsible,” it’s mathematically powerful.

4) The small business owner who sees rates as a hiring decision

Small business owners often describe interest rates in plain terms: “Can I afford to expand?” A higher-rate environment can turn a new equipment loan or a

line of credit into something you debate for weeks instead of signing in an afternoon. That hesitation can translate into slower hiringeven if business demand

is decentbecause cash flow has less cushion. When borrowing costs ease, confidence can return, but it’s rarely instant; owners want to see stability, not a

single rate headline. This is one reason unemployment can lag changes in interest rates.

5) The household that feels fine on paper but tight in practice

A very modern experience is being employed, paying the mortgage on time, and still feeling financially stressed. The reasons are usually a mix: higher everyday

costs than a few years ago, higher borrowing rates than people got used to, and the reality that not everyone’s wages rise at the same pace.

Many households respond by refinancing only when it clearly works, prioritizing high-interest debt, and building a slightly larger emergency buffer so a surprise

expense doesn’t automatically become a 23% APR problem. The humor in itif you need anyis that “adulting” sometimes means you’re basically managing a tiny central

bank at home: balancing risk, liquidity (cash), and inflation (grocery prices), with fewer economists and more laundry.