Table of Contents >> Show >> Hide

- Why Everyone Kept Expecting a Recession

- So… Did the Recession Actually Happen?

- What the Data Says the Economy Was Doing Instead

- Why the Recession Didn’t Show Up (Yet): The Big Explanations

- Recession Indicators: Which Ones Lied, and Which Ones Behaved?

- “It Still Feels Like a Recession” Why That’s Not Crazy

- Where the Recession Could Still Come From

- What to Do With This Information (Without Panic-Buying Canned Beans)

- of “Recession” Experiences (Because the Vibes Have a Point)

Remember the recession we were all “definitely” going to have? The one that was basically scheduled like a dentist

appointment“See you in Q4!”and then never showed up?

For a while, it felt like the U.S. economy was starring in a suspense movie where the monster is always “just off

screen.” Interest rates surged, inflation burned hot, the yield curve did that upside-down thing economists treat

like a horror-movie violin sting… and yet the big “R” word kept getting delayed like a flight on a foggy morning.

So what happened to the recession? Short version: parts of the economy slowed, but the broad collapse never became

the main plot. The longer version is more interestingbecause it explains why “recession vibes” can feel real even

when the official data doesn’t wave a white flag.

Why Everyone Kept Expecting a Recession

1) The Fed hit the brakeshard

Historically, rapid rate hikes are the economic equivalent of slamming the brakes on a highway: the goal is to stop

inflation, but it can also toss passengers (jobs, spending, confidence) around the cabin. Many analysts assumed that

tightening financial conditions would eventually crack consumer demand and business investment.

2) Old-school indicators started screaming

A few traditional recession signals flashed red:

-

The yield curve inversion: When short-term rates rise above long-term rates, it has often preceded

recessions. It doesn’t guarantee one, but it’s a classic warning light. -

Leading indicators weakened: Composite indexes designed to foreshadow downturns showed persistent

softening. -

Sentiment tanked: Consumers and businesses sounded gloomy even while spending and hiring stayed

surprisingly resilient.

3) Inflation was painfuland pain changes behavior

Even after inflation cooled, the price level stayed higher than people were used to. Grocery aisles felt like

a prank. Rent felt like a monthly mugging. And when households feel squeezed, it’s natural to assume a recession is

nexteven if the economy is still expanding on paper.

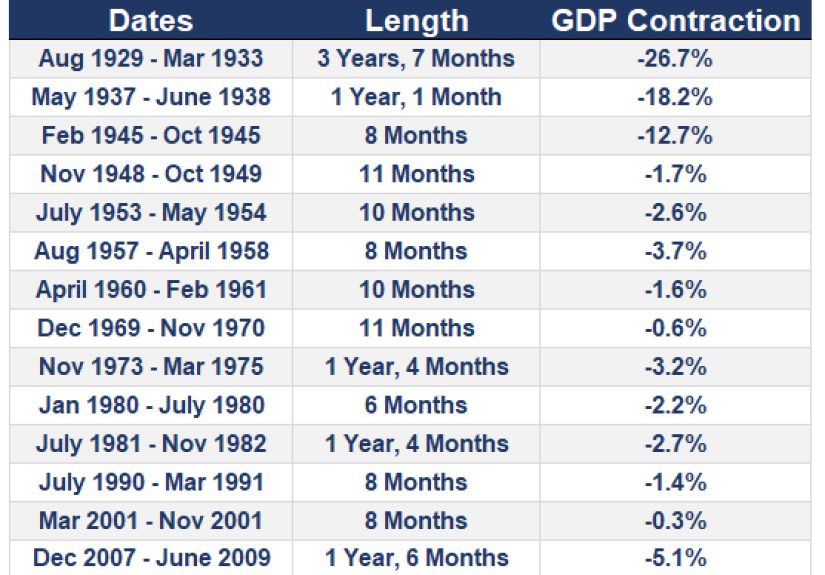

So… Did the Recession Actually Happen?

Not in the official, economy-wide sense

In the U.S., “recession” isn’t declared by vibes or two quarters of GDP trivia. It’s dated after the fact by the

National Bureau of Economic Research (NBER), which looks for a significant, broad, and lasting decline across the

economythings like employment, income, spending, production, and sales.

As of early 2026, the most recent recession the NBER has on its books remains the sharp pandemic downturn in early

2020. That doesn’t mean the economy felt great the whole timejust that it didn’t meet the threshold for an

economy-wide contraction.

But some sectors had a “rolling recession” feel

A key twist: the economy didn’t move in a single herd. Instead, different sectors took turns being miserable.

- Housing got punched by higher mortgage rates.

- Interest-rate-sensitive business investment cooled.

- Some manufacturing softened while services kept trucking.

- Parts of tech went through layoffs and belt-tightening.

If your industry was in the “down” part of the rotation, it absolutely felt recession-y. But other parts of the

economyespecially services and large segments of consumer spendingkept the overall engine running.

What the Data Says the Economy Was Doing Instead

Growth didn’t vanish

Economic growth cooled at times, then re-accelerated, then cooled againmessy, yes, but not a broad contraction.

Real GDP growth remained positive in key periods, including a strong annualized pace reported for Q3 2025.

Unemployment rose a bitbut didn’t spike

Recessions usually come with a notable jump in joblessness. Instead, unemployment drifted higher from very low levels,

but remained far from the kind of sharp surge that historically marks a downturn. Hiring slowed in places, but the

labor market avoided a full-on collapse.

Inflation cooled without the economy cratering

The most surprising chapter of this story is disinflation with continued expansion. Inflation fell a lot from its

peak, helped by easing supply chain pressures, improving goods availability, and slower (but not dead) demand.

That “soft landing” outcomelower inflation without a deep recessionwas the unicorn scenario. It didn’t show up

perfectly, but it showed up enough to change the narrative.

Why the Recession Didn’t Show Up (Yet): The Big Explanations

1) The inflation problem wasn’t purely “too much demand”

A major chunk of post-pandemic inflation was fueled by supply disruptions (shipping delays, shortages, production

bottlenecks) and a rapid rotation in what people bought. When supply improved, inflation could fall without the Fed

needing to “break” the economy.

Translation: if inflation is partly a supply story, disinflation can also be partly a supply fixnot only a demand

collapse.

2) Households had cushionsthen adapted

Early on, many households had excess savings from pandemic-era support and reduced spending opportunities. Over time,

that cushion fadedand research suggested it was largely spent down by 2024. Yet consumer spending didn’t simply

disappear. People adjusted: they traded down, switched brands, shifted spending categories, took second jobs, and

generally kept the wheels turning.

3) “Locked-in” low rates delayed the pain

In past cycles, rate hikes hit households quickly through adjustable-rate mortgages and frequent refinancing.

This time, many homeowners were sitting on fixed-rate mortgages locked in at historically low rates.

The result: higher interest rates absolutely mattered, but the transmission was slower and uneven. Instead of a

sudden economy-wide gut punch, the impact spread graduallyharder on new buyers, renters, and businesses that rely

on short-term borrowing.

4) Productivity improved in key stretches

Productivityhow much output workers produce per hourmatters because it can let the economy grow without stoking

as much inflation. Stronger productivity can also help firms absorb higher wages without raising prices as aggressively.

In late 2025 data, productivity growth showed notable strength, and commentary increasingly tied part of that

improvement to investment in technology and process upgrades (including AI-related investment). If productivity rises,

you can get a weird-but-welcome mix: growth that doesn’t require hiring like crazy, plus some relief on unit labor costs.

5) “Recession probability” isn’t “recession destiny”

Models like the New York Fed’s yield curve framework estimate the probability of a recession ahead, not a guarantee.

In recent years, those probabilities rose and felland some indicators generated false alarms.

The practical takeaway: recession forecasting is a game of probabilities, and the post-pandemic economy has been a

chaos monkey that enjoys knocking over neat historical patterns.

Recession Indicators: Which Ones Lied, and Which Ones Behaved?

The yield curve: still useful, but not a stopwatch

The yield curve has an impressive track record, but it can be early, and it can be distorted by global demand for

U.S. Treasuries, shifting inflation expectations, and central bank balance sheet dynamics. It’s a warning lightnot

a countdown timer.

The Sahm Rule: the “tell me when jobs break” signal

The Sahm Rule looks for a meaningful rise in unemployment relative to its recent low. It’s designed as a timely

recession flag once labor market deterioration becomes clear. In this cycle, unemployment rose, but not in the kind

of sharp, fast way that typically triggers that signal.

Leading indexes: pessimistic, but cooling pessimism

Composite leading indicators stayed soft for a long time, suggesting elevated risk. But the pace of deterioration

moderated at points, consistent with an economy slowing without necessarily tipping into contraction.

“It Still Feels Like a Recession” Why That’s Not Crazy

Prices stayed high even when inflation cooled

Falling inflation means prices are rising more slowlynot that they roll back to what they were. If your grocery bill

jumped 25% over a couple years, “good news, it’s only going up 3% now” is not emotionally satisfying. That gap between

macro data and household reality is a big reason the recession narrative lingered.

Higher rates created “two economies”

If you already owned a home with a low fixed-rate mortgage, you might have felt relatively insulated. If you were trying

to buy, refinance, or start a business with new borrowing costs, the economy felt like it suddenly started charging

cover at the door.

Job market churn is scarier than unemployment stats

Even with low-ish unemployment, workers can feel uneasy if hiring slows, layoffs rise in visible industries, or wage

growth cools. The economy can be expanding while the job hunt gets harderespecially for career switchers and new grads.

Where the Recession Could Still Come From

“No recession yet” isn’t the same as “invincible forever.” Risks that can still tip the economy include:

- Sticky services inflation that keeps policy tight longer than markets hope.

- Credit stress (delinquencies, tighter lending standards) spreading beyond pockets of weakness.

- Commercial real estate and refinancing risk in a higher-rate world.

- Fiscal uncertainty and policy shocks that hit business confidence or household budgets.

- Global surprises (energy spikes, supply disruptions, geopolitical events).

In other words: the recession didn’t vanish into a wormhole. It just didn’t win the timeline so far.

What to Do With This Information (Without Panic-Buying Canned Beans)

1) Treat forecasts as probabilities, not prophecies

A 35% recession probability is meaningfulbut it’s also a 65% chance of no recession. Plan like an adult, not like a

doomsday influencer.

2) Build resilience, not doom

Emergency savings, manageable debt, and flexible spending plans aren’t just “recession prep.” They’re life prep.

3) Watch labor markets more than headlines

If unemployment begins rising quickly and broadly, the story can change fast. Jobs tend to be the tipping point where

“slowdown” becomes “recession.”

of “Recession” Experiences (Because the Vibes Have a Point)

Even when the macro charts say “expansion,” lived experience can be a different genre. Here are a few composite,

real-world-style snapshots that explain why people kept asking, “Isn’t a recession supposed to be here by now?”

Experience #1: The grocery store math problem

A parent stands in the cereal aisle doing mental gymnastics: “Okay, this box used to be $3.49, now it’s $5.99, and

my teenager eats cereal like it’s a competitive sport.” Inflation cooling doesn’t bring back the old prices, so the

household budget still feels permanently stressed. The result is a constant low-level alarm: fewer extras, more store

brands, and the strange feeling of being “fine” financially while also feeling like you’re one surprise car repair

away from chaos.

Experience #2: The housing market optical illusion

A couple wants to buy their first home. They show up with good jobs, decent credit, and optimismonly to discover

that higher mortgage rates can turn an “affordable” listing into a monthly payment that looks like a luxury product.

Meanwhile, their friend who bought in 2021 is paying a lower mortgage and casually renovating a kitchen. Same economy.

Totally different reality. One group feels stuck; the other feels mostly sheltered. That split makes “recession talk”

feel plausible even without job losses everywhere.

Experience #3: The small business tightrope

A café owner notices customers still coming inbut ordering one pastry instead of two, or skipping the fancy latte.

Costs stay elevated, especially for labor and rent. Loans are more expensive than they used to be, so expanding or

remodeling gets postponed. Nothing is collapsing, but the margin for error gets thinner. The business survives by

getting more efficient, raising prices carefully, and praying that the espresso machine doesn’t choose violence this

month. It’s not a recession, but it’s not exactly a victory lap either.

Experience #4: The “job market is fine” asterisk

Someone with a stable job hears “the labor market is strong” on the news, then watches a friend apply to 120 roles

and get ghosted by half of them. Hiring can slow without unemployment exploding, and that’s enough to change behavior:

fewer big purchases, more caution, and a renewed love for updating résumés at 1 a.m. The economy can be growing while

the job search feels like speed dating with an invisible audience.

Experience #5: The investor whiplash

Markets spent years bouncing between “recession is imminent” and “soft landing achieved.” One month, investors pile

into safe assets. The next, they chase growth again. For ordinary people, the emotional toll is less about portfolio

theory and more about uncertainty: “Should I hold cash? Should I buy? Should I do nothing and pretend I’m above it

all?” The recession that didn’t arrive still extracted a payment in stress, because uncertainty has its own

subscription fee.

Put together, these experiences explain the paradox: the recession didn’t officially happen, but the economy still

asked a lot of people to live like it might. That’s the era we’ve been inless “collapse,” more “constant recalibration.”