Table of Contents >> Show >> Hide

- Why “High Income” Is a Moving Target

- Benchmark #1: High Income as “Top of the Distribution”

- Benchmark #2: High Income as “Upper Income”

- Benchmark #3: High Income as “Comfortable After Local Costs”

- Gross Income vs. Take-Home Pay: The Plot Twist Everyone Forgets

- High Income Doesn’t Automatically Mean High Wealth

- What a “High Income” Can Look Like: Three Realistic Scenarios

- How to Tell If Your Income Is High (Without Needing a Hotline)

- Common Myths About High Income (That Deserve a Time-Out)

- How High Earners Stay Comfortable (Instead of Accidentally Becoming Broke-Adjacent)

- Conclusion: So, What’s a High Income?

- Bonus: Experiences That Show What “High Income” Really Feels Like (500+ Words)

“High income” sounds like a simple questionuntil you try to answer it without starting an argument at a barbecue.

In the U.S., the definition can change depending on who’s asking, where they live, and whether they’re staring at

a daycare bill the size of a used car.

Here’s the honest truth: high income is both a number and a feeling. It’s a number when you compare

yourself to everyone else (percentiles). It’s a feeling when your paycheck hits and your rent immediately sprints

away like it’s late for a meeting.

This guide breaks it down in a practical, U.S.-specific wayusing clear benchmarks, real-world examples, and a bit

of humor to keep things from turning into a spreadsheet-induced nap.

Why “High Income” Is a Moving Target

There isn’t one official sign that flashes “CONGRATS, YOU’RE HIGH INCOME” the moment your salary crosses a line.

Instead, high income is usually defined in three overlapping ways:

- Relative: You earn more than most people (top 10%, top 5%, etc.).

- Class-based: You’re considered “upper income” (often based on household size).

- Lifestyle-based: Your income comfortably covers local costs and allows saving, investing, and breathing.

If you want a definition that actually holds up in real life, you’ll use all three.

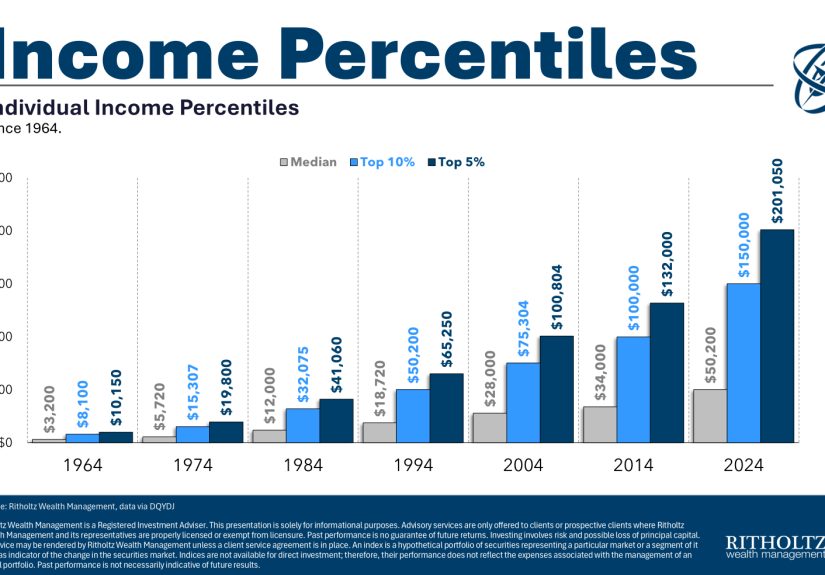

Benchmark #1: High Income as “Top of the Distribution”

One straightforward way to define high income is: you’re in the top slice of U.S. households.

That’s useful because it’s apples-to-apples across the countryat least in theory.

So… what counts as “top 10%” in the U.S.?

Recent national income distribution data shows that the 90th percentile household income is roughly

in the quarter-million-dollar range (and higher for family households). Put simply: if your household

income is somewhere around that neighborhood, you’re no longer “above average.” You’re above most.

Want an even tighter definition? Many people mentally label “high income” as top 5%. That’s where things begin to

look like: “Okay, this household can max retirement accounts, take vacations, and still replace a water heater

without a dramatic monologue.”

Important: household income isn’t the same as your salary

A household can include one earner, two earners, a side hustle, investment income, and that one rental property

Uncle Mike insists is “basically passive” (it’s not). So if you’re comparing your salary to household percentiles,

keep the units consistentor at least acknowledge the mismatch.

Benchmark #2: High Income as “Upper Income”

Another popular yardstick is the “upper-income” cut-off used by researchers and media. This approach is especially

helpful because it adjusts for household size. A single adult making $150,000 and a household of five

making $150,000 do not live the same life. One is deciding between Tesla trim packages; the other is deciding which

kid gets the last string cheese.

A quick, practical rule of thumb

If your household income is well above the middle-income range for your household size, you’re

usually considered upper income. Nationally, the “upper income” threshold for a three-person household lands in the

high-$100Ks (in inflation-adjusted terms), and it rises as household size increases.

This method is less about bragging rights and more about context: it helps explain why “six figures” can feel

comfortable for one household and tight for another.

Benchmark #3: High Income as “Comfortable After Local Costs”

Here’s where the internet fights start. Because the moment you bring up cost of living, someone will say:

“I make $110K in my city and feel broke.” And someone else will reply:

“I make $65K where I live and feel fine.” And both can be correct.

A lifestyle-based definition asks a better question:

After taxes and essential costs, do you have room to save, invest, and handle surprises?

Living wage vs. high income

Tools that estimate a living wage focus on meeting basic needshousing, food, transportation,

health care, and childcarebased on local prices and household type. That’s the floor. A “high income” is what you

get when you’re comfortably above that floor and can consistently build wealth.

Another “modest but adequate” lens is family budget modeling, which estimates what a household needs for a basic,

stable standard of living in a specific county or metro area. Again: that’s not “rich.” That’s “not one emergency

away from chaos.”

Example: the same income, wildly different outcomes

-

Single adult, lower-cost region: $120,000 can feel genuinely high incomestrong savings rate,

flexibility, faster wealth-building. -

Two adults + two kids, high-cost metro: $220,000 may still feel tight once housing, childcare,

insurance, commuting, and taxes take their turns. -

Single parent with childcare needs: “High income” can require a larger cushion because childcare

behaves like a second rent with snack fees.

Gross Income vs. Take-Home Pay: The Plot Twist Everyone Forgets

If you want to know whether you’re actually high income in practice, stop staring at your gross salary like

it’s a motivational poster. Start looking at:

after-tax income + benefits + unavoidable costs.

Taxes: marginal vs. effective (a.k.a. “no, your whole income isn’t taxed at 24%”)

Federal income taxes are progressive, meaning your income is taxed in layers (brackets). As your income rises,

additional dollars may be taxed at higher marginal rates, but your overall effective rate will be lower than your

top bracket. This matters because people often overestimate how much taxes “eat” their incomethen underestimate

how much lifestyle creep quietly finishes the job.

Also, payroll taxes, state taxes, and local taxes can change the picture a lot. Two households with the same gross

income can have different take-home pay depending on where they live and how they’re paid (W-2 vs. self-employed,

bonuses, stock comp, etc.).

High Income Doesn’t Automatically Mean High Wealth

High income is powerful, but it’s not magic. It’s entirely possible to earn a lot and still feel financially

stressed if:

- your fixed costs are massive (big mortgage, expensive cars, high childcare),

- your income is volatile (commission-heavy, seasonal, startup equity),

- you’re carrying expensive debt (credit cards, private loans), or

- you’re supporting extended family or paying for medical needs.

Wealth is what happens when income is converted into assets over time. National financial surveys consistently show

that wealth is distributed far more unevenly than incomemeaning “high income” and “high wealth” overlap, but they

are not the same club.

What a “High Income” Can Look Like: Three Realistic Scenarios

1) The early-career high earner (a.k.a. “I finally made itwhy am I still anxious?”)

Salary: $140,000. Student loans: still present. Rent in a hot market: aggressive. Retirement savings: “I’ll start

next year” (famous last words). This person is high income in many places, but without a plan, it won’t feel like it.

2) The dual-income household that’s truly comfortable

Two earners. Solid benefits. Moderate housing costs. They can save 15–25% of take-home pay, cover car repairs

without panic, and still take vacations. This is what “high income” often means in everyday terms:

margin.

3) The high-income household in a high-cost area (a.k.a. “We make WHAT and still pack lunch?”)

Household income: $280,000. Housing: expensive. Childcare: expensive. Insurance: expensive. Taxes: also not a fan.

They’re high income by national percentiles, but their lifestyle is “comfortable middle class” locally. This is why

location matters so much.

How to Tell If Your Income Is High (Without Needing a Hotline)

Here’s a quick checklist that works better than arguing about whether $100K is “a lot.”

The five tests

- Essentials test: Can you pay housing, food, transportation, utilities, and health costs without juggling bills?

- Savings test: Can you consistently save/invest at least 15% of your income (more if you’re behind)?

- Emergency test: Could you handle a $2,000–$5,000 surprise without debt?

- Future test: Are you on track for retirement (not just “hoping” for retirement)?

- Flexibility test: Could you absorb a job loss or pay cut without immediate crisis?

If you’re checking these boxes and your income is well above local “basic needs” costs, you’re living the

practical definition of high income: you have options.

Common Myths About High Income (That Deserve a Time-Out)

Myth: “Six figures is rich.”

Six figures is a milestone, not a universal lifestyle. In some places it’s “nice.” In others it’s “nice, but

please don’t look at home prices.”

Myth: “If you make a lot, budgeting is optional.”

High income can hide bad money habits for a while, but it can’t make them disappear. Lifestyle creep loves high

earners because it arrives dressed as “You deserve it.”

Myth: “Taxes take everything.”

Taxes can be substantial, but the bigger threat for many high earners is uncontrolled fixed costsespecially

housing and car paymentsbecause they don’t stop when the bonus does.

How High Earners Stay Comfortable (Instead of Accidentally Becoming Broke-Adjacent)

The goal isn’t to “feel rich.” The goal is to build a financial life that doesn’t fall apart when your furnace

breaks, your kid needs braces, or your company decides to “restructure” (corporate code for “surprise!”).

A simple framework that actually works

Many people start with a budget split like 50/30/20 (needs/wants/savings). High-cost realities sometimes push the

“needs” share higher, so the key is not the exact ratioit’s the principle:

pay yourself first, automate savings, and keep fixed costs from eating your future.

Three high-income moves that punch above their weight

- Cap fixed costs: The smaller your required monthly spend, the more powerful your income becomes.

- Automate investing: Wealth-building should happen on autopilot, not based on willpower.

- Use windfalls wisely: Bonuses and stock payouts are great for catching upretirement, emergency fund, debt payoff.

High income is most valuable when it buys you one thing money can actually buy: control.

Control over time, stress, choices, and the ability to say “no” when needed.

Conclusion: So, What’s a High Income?

A high income is best understood as a mix of benchmarks:

earning more than most households nationally, qualifying as upper income for your household size,

and having enough after-tax margin to save, invest, and live comfortably where you are.

If you want a simple, useful takeaway, it’s this:

High income isn’t just “big money.” It’s money that creates margin.

Margin to handle life, fund your goals, and build a future that doesn’t depend on everything going perfectly.

Bonus: Experiences That Show What “High Income” Really Feels Like (500+ Words)

Numbers are helpful, but “high income” often shows up as a set of experienceslittle moments that reveal whether

your income is giving you options or just giving you more expensive problems. Below are a few composite stories

that reflect what many Americans describe when they talk about crossing into “high income” territory.

The “I hit six figures and expected confetti” experience

This one is classic: someone lands a job paying $110,000–$140,000 and expects instant comfort. Instead, they notice

something awkwardlife doesn’t automatically get cheaper just because they make more. They upgrade a few things

(a nicer apartment, better coffee, more dinners out), and suddenly the extra income feels… already assigned.

The emotional whiplash comes from realizing that income increases quickly, but financial security builds slowly.

The turning point is usually when they automate savings and stop letting their lifestyle expand to match every raise.

Once they consistently invest and keep fixed costs reasonable, the same income starts to feel dramatically “higher.”

The “high income, high cost of living” experience

A couple earns $240,000–$320,000 combined in a high-cost metro. On paper, it’s undeniably high income. In daily

life, it’s… complicated. Housing is a large, non-negotiable number. Childcare competes with the mortgage like it’s

trying to win a trophy. Insurance premiums show up like uninvited party guests. This household learns the

difference between “high income” and “high flexibility.” Their breakthrough comes when they treat fixed costs as a

strategic decision instead of a lifestyle statement. A slightly smaller home or one less car payment can create

breathing room that feels like a raise without needing a raise.

The “first real emergency fund” experience

Many people describe a specific moment when they finally feel “high income,” and it’s not when they buy something

flashy. It’s when they realize they can handle a surprise expense without panic. The car needs a $1,800 repair,

the dog eats something suspicious, or the water heater retires without noticeand instead of fear, the reaction is:

“Annoying… but fine.” That shift is huge. It’s the first time money stops being purely reactive and starts becoming

proactive. This is also when people begin to value boring things like sinking funds, insurance deductibles, and

automated transfers. (Yes, adulthood is thrilling.)

The “we’re high income, so why are we stressed?” experience

High income can still feel stressful when income is volatile. Think commission-based sales, contract work, or

equity-heavy compensation. The household may have strong yearly earnings but uneven monthly cash flow. They can

feel “rich” one month and anxious the next. The most common solution is building a bigger cash buffer than

traditional advice suggestssometimes six to twelve months of expensesand separating “baseline living” from

“bonus living.” In other words: live on the predictable part, and treat the unpredictable part as a tool for goals

(investing, debt payoff, future big purchases) rather than a reason to permanently raise spending.

The “high income finally buys time” experience

The best version of high income isn’t a luxury itemit’s reduced friction. It’s being able to pay for help in the

season of life when time is scarce: occasional house cleaning, grocery delivery, reliable childcare, a car that

doesn’t constantly need repairs. People often describe this as the moment their income becomes “high” in a way that

matters. Not because they’re living extravagantly, but because they’re buying back hours and lowering stress.

When high income creates time, it’s doing its job.

Across these experiences, the theme is consistent: high income feels high when it creates margin

margin in your budget, margin in your schedule, and margin in your ability to handle life without spiraling.

That’s the real definition most people are reaching for, even when they think they’re asking about a number.